The Same Thing – Over and Over

Each quarter, we send clients a letter, along with performance reports that detail our results net of all fees as compared to various indices and investment policy benchmarks.

To provide transparency into our process and current views, the following is an excerpt from our most recent quarterly commentary. It includes a quote from Benjamin Graham and thoughts from Jason Zweig, which were the inspiration for the title of this post.

As has happened many times before, I am writing a quarterly letter as the market is experiencing large swings. These swings increase emotion among investors and can create concern (click here for more on this in a piece we wrote around this same time in 2015).

Similar to what we mentioned in our last letter, some of the market moves are happening due to concerns about the possibility of rising interest rates. We take this seriously, as rising rates may create stock and bond market headwinds.

We also strive to remain humble, however, about the long-term benefits of any short-term tactical moves that we contemplate, net of all taxes and expenses. The reason why is that history continues to show that even the most accurate forecasters on Wall Street can be quite Fallible.

This doesn’t mean that we do not take into account differing opinions.

We review new research virtually every day from a multitude of sources, and evaluate and debate it in conjunction with our Research Roundtable and our greater network of industry colleagues.

As an example, we have been diving deeper into what the evidence says is the best way to position portfolios in rising rate environments. One of the most robust papers we studied evaluated the relationship between inflation and 23 asset classes and strategies over the seventy-three year period from 1927-2000.

We wrote about this study recently in a piece we titled Inflation – What Should An Investor Do?

Here’s what the authors of the research paper found:

“The right mix of assets for growth and hedging purposes ultimately depends on an investor’s goals and needs. The good news is that most of the global assets we study have been able to outpace U.S. inflation over the long term. Hence, simply staying invested may by itself be an effective long-term solution to inflation concerns.”

Put another way…

The best long-term strategy to manage through inflationary periods is to stick to your long-term strategy.

Encouraging clients to stick to their long-term plans, yet again, reminds me of something that Jason Zweig of the Wall Street Journal wrote about his job back in 2013:

“My job is to write the exact same thing… in such a way that… I am [not] repeating myself.”

Jason’s message is always the same and aligns with the quote below from the person whom many consider to be the father of modern security analysis, Benjamin Graham:

“The investor’s chief problem – and even his worst enemy – is likely to be himself.”

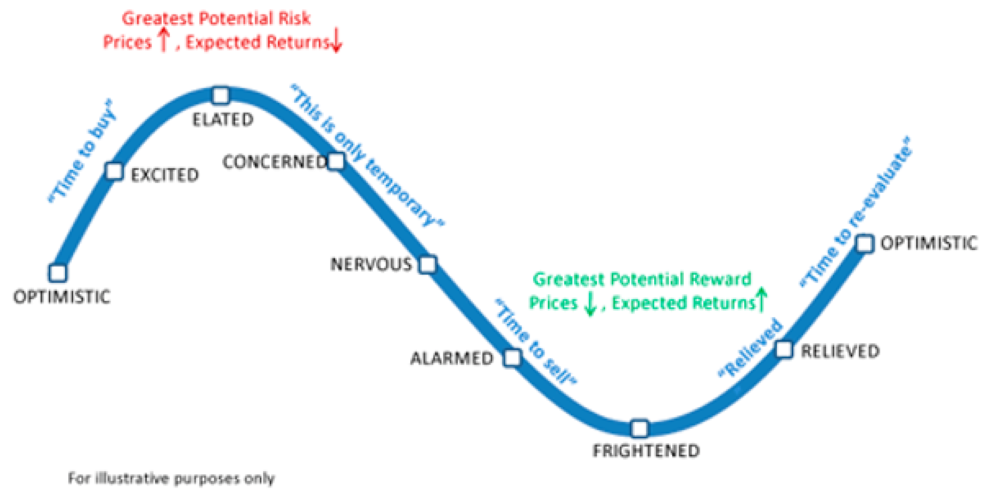

We have never met an investor who is totally immune to the problems associated with the Cycle of Market Emotions (professionals included), which is why we regularly repeat, even to ourselves, much of what we’ve said before.

In an effort to avoid overreacting to market swings or ever changing forecasts, we stay anchored on a process that is linked to goal oriented investment policy statements.

This strategy focuses us on rebalancing positions to stay in line with investment policies, which mandate that we buy after large drops if we find ourselves too far below allocation targets and trim positions after large market runs if we move too far ahead of targets.

I know that this might sound overly simplistic, but as Warren Buffett has said…

“Investing is simple, but not easy.”

Related to this, we’d love to say that, after the uneasiness we all felt surrounding the historic market drop in March of 2020, we were correctly forecasting the subsequent historic market rise when we started buying stocks and other risk assets in April 2020.

As I wrote in our Q1 and Q2 2020 letters, though, we were just following the evidence about historical market movements and sticking to our process.

We will certainly not get buys or trims right every time and we will make mistakes.

Going forward, though, we will continue to stay focused on what the evidence consistently says about the advantages of Simple Alternatives and recall the words of the late David Swensen, the long-time Chief Investment Officer of Yale:

“Only extraordinary circumstances justify deviation from a simple strategy…”

_____________________________________________________________________

Related Reading:

{kind=link}

The Difference Simple Alternatives Can Make – 15 for 15

The Difference Simple Alternatives Can Make – 15 for 15  The Road Less Traveled – Simple Alternatives

The Road Less Traveled – Simple Alternatives  Are Most Investment Managers One Hit Wonders?

Are Most Investment Managers One Hit Wonders?